The UAE’s corporate tax framework has changed how Free Zone businesses operate. While Free Zones remain tax-friendly, only companies that meet strict conditions can keep the 0% rate under the Qualifying Free Zone Person (QFZP) regime.

For founders, investors, and finance managers, understanding what defines a QFZP is essential. It determines whether profits are taxed at 0% or 9%, and sets out what compliance steps are required to maintain eligibility.

What Is a Qualifying Free Zone Person?

A Qualifying Free Zone Person is a company registered in a UAE Free Zone that earns certain types of income qualifying for a 0% corporate tax rate, while non-qualifying income is taxed at 9%.

To keep this benefit, a QFZP must:

- Have real business substance within the Free Zone.

- Maintain audited financial statements.

- Conduct only approved qualifying activities.

- Comply with transfer pricing and other tax documentation rules.

If a company fails any of these conditions, it loses its QFZP status and becomes subject to the standard 9% corporate tax rate.

Legal Basis for the QFZP Regime

The concept of the QFZP was introduced under Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses. Key clarifications were later added through several ministerial decisions:

- Cabinet Decision No. 100 of 2023: Defined qualifying income, Free Zone–to–mainland transactions, and property-related rules.

- Ministerial Decision No. 229 of 2025: Updated the lists of qualifying and excluded activities and refined the “de minimis” threshold.

- Ministerial Decision No. 230 of 2025: Specified recognised price reporting agencies for commodity traders.

- Ministerial Decision No. 84 of 2025: Made audited financial statements mandatory for all QFZPs starting January 2025.

These updates aim to align the UAE’s Free Zone benefits with global tax standards while maintaining the country’s competitiveness.

Eligibility Criteria: How to Qualify from Day One

To benefit from the 0% rate, a company must satisfy all conditions from the start of its tax period.

1. Real Substance in the Free Zone

A QFZP must demonstrate genuine business operations—having staff, premises, and expenses in the Free Zone that reflect actual economic activity. “Paper” or virtual entities without substance do not qualify.

2. Audited Financial Statements

All QFZPs must prepare audited financial statements, regardless of size or revenue. These statements confirm income types and ensure the business meets compliance standards.

3. Arm’s-Length Transactions

Deals between related parties must follow transfer pricing rules. Prices must reflect market value and be supported by documentation.

4. Electing In or Out of the Regime

A Free Zone company can choose to opt out of the 0% regime and be taxed at 9% on all income. Once it opts out, it cannot reapply for QFZP status for five tax periods.

Corporate Tax Rates: What Falls Under 0% vs. 9%

The key difference lies in the source and nature of income.

Qualifying Income (0% Tax)

- Transactions between two Free Zone entities.

- Approved qualifying activities listed under Ministerial Decision 229 of 2025.

- Certain intellectual property income developed with real R&D.

Non-Qualifying Income (9% Tax)

- Revenue from excluded activities, such as banking, conventional insurance, and real estate leasing outside Free Zones.

- Sales to individuals (natural persons), except in limited cases like ship or aircraft leasing.

Unlike mainland businesses, QFZPs cannot use the AED 375,000 small business exemption—their 0% rate applies only to qualifying income.

Qualifying and Excluded Activities

Understanding which activities count is central to QFZP eligibility.

Qualifying Activities Include:

- Manufacturing and processing of goods.

- Trading of qualifying commodities (such as metals, energy, and agricultural products).

- Reinsurance and fund management services.

- Headquarters, treasury, or financing services provided to related parties.

- Aircraft and ship leasing or operation.

- Distribution of goods in or from a Designated Zone, provided distribution rules are met.

- Logistics and related support functions.

Commodity traders must use prices from recognised agencies such as Platts, Argus, ICIS, or ICE.

Excluded Activities Include:

- Retail or other transactions with natural persons (except for specific exceptions).

- Banking and conventional insurance.

- Ownership or leasing of property outside a Free Zone.

- Financing and leasing other than approved treasury or aircraft activities.

If most of a company’s income comes from excluded activities, it cannot maintain QFZP status.

Serving the UAE Market: When 0% Still Applies

A Free Zone business can deal with mainland clients, but not all income will qualify for the 0% rate.

- Mainland branches of Free Zone companies are taxed at 9% on their profits.

- Some qualifying activities—like logistics, manufacturing, or aircraft leasing—may still attract 0% even when serving mainland customers, as long as the activity remains on the approved list.

For distribution, the goods must:

- Enter the UAE through a Designated Zone, and

- Be sold to a reseller, processor, or a public benefit entity—not directly to consumers.

The De Minimis Rule: Keeping Non-Qualifying Income in Check

The de minimis threshold ensures that most of a QFZP’s revenue comes from qualifying activities. Under current rules:

- Non-qualifying income must stay below 5% of total revenue or AED 5 million, whichever is lower.

- Non-qualifying income includes both excluded activities and other income not meeting qualifying criteria.

If the threshold is breached, the company loses its QFZP status from the start of that tax period and for the next four tax periods. This effectively disqualifies the business for up to five years.

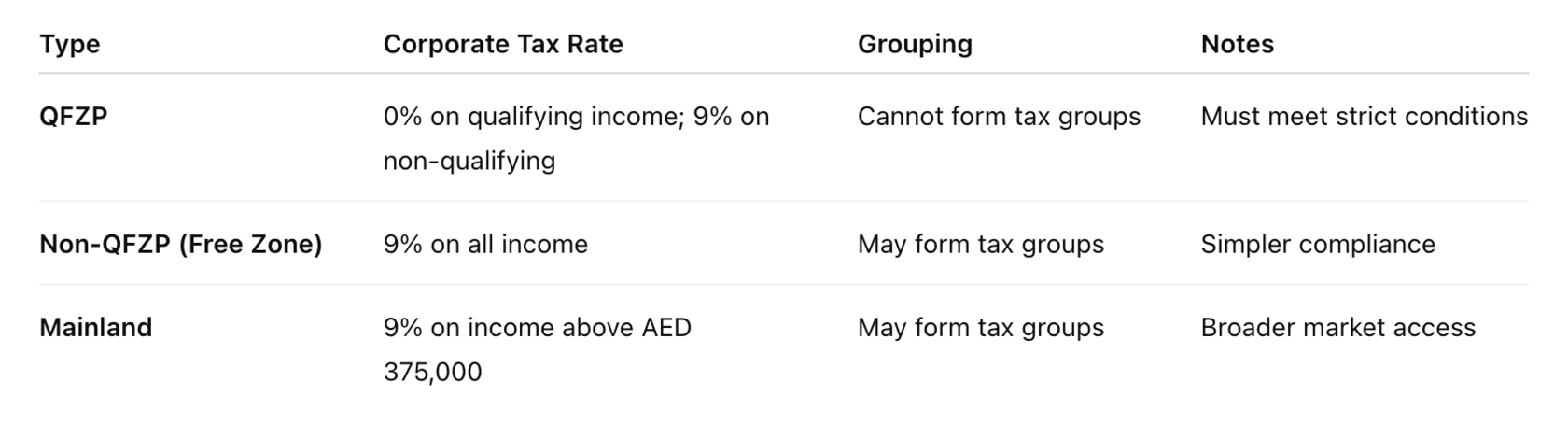

QFZP vs. Non-QFZP vs. Mainland Companies

While QFZPs enjoy lower taxes, compliance is heavier. Mainland or non-QFZP setups may be more practical for retail, banking, insurance, or property development.

Compliance and Reporting Essentials

From 2025 onward, all Free Zone companies must register for corporate tax and file returns within nine months after the end of their financial year.

Key obligations include:

- Preparing audited financial statements.

- Keeping detailed documentation for income classification.

- Filing transfer pricing disclosures if related-party thresholds are met.

- Maintaining an audit trail of contracts and transactions.

Consistent documentation is crucial because even minor errors can lead to losing 0% eligibility.

Self-Assessment: Do You Qualify as a QFZP?

To check eligibility, apply this five-part framework:

- Location Test: Must be legally incorporated and licensed in a UAE Free Zone.

- Activity Test: Must conduct one or more qualifying activities as listed in the law.

- Substance Test: Must have real operations, staff, and expenses within the Free Zone.

- Compliance Test: Must follow audit, transfer pricing, and filing requirements.

- Revenue Mix Test: Non-qualifying income must remain within the de minimis limit.

Failing any of these tests means the business is treated as a regular taxpayer at 9%.

Common Misunderstandings About QFZP Rules

- “Being in a Free Zone automatically means 0% tax.”

- False. Companies must meet all QFZP conditions to qualify.

- “Online B2C sales are always tax-free.”

- False. Sales to natural persons are excluded from qualifying income.

- “All intellectual property income qualifies.”

- False. Only IP developed through genuine R&D and managed from the Free Zone qualifies.

Summary

The Qualifying Free Zone Person framework is central to how corporate tax applies across the UAE’s Free Zones. It preserves 0% benefits for businesses that create real economic value and follow clear compliance standards.

For companies that rely on Free Zone advantages, staying informed and structured is key. Meeting substance, audit, and reporting requirements ensures that the 0% rate remains both valid and sustainable.

FAQs

Can foreign investors own a QFZP?

Yes. Foreign ownership is permitted as long as all QFZP conditions are met.

Can a QFZP sell to mainland clients and still get 0%?

Yes, but only for qualifying activities such as logistics or manufacturing under set conditions.

What happens if a company exceeds the de minimis threshold?

It loses QFZP status for that tax period and the next four.

Do small Free Zone firms need audited accounts?

Yes. From January 2025, audited financial statements are mandatory for all QFZPs.